Goods and Services Tax |

What is Goods and Services Tax?

GST which is also known as VAT or the value added tax in many countries is a multi-stage

consumption tax on goods and services. The Malaysian government had announced on the 25th

October 2013 that it will be implemented on 1st April 2015 at a rate of 6%. Payment of tax

is made in stages by intermediaries in the production and distribution process. The tax

itself is not a cost to the intermediaries since they are able to claim back GST incurred

on their business inputs. GST is imposed on goods and services at every production and

distribution stage in the supply chain including importation of goods and services.

|

Do I need to register my business under GST?

Those with annual sales of taxable supply exceeding the prescribed threshold of RM500,000

are mandatorily required to be registered. However, those below the prescribed threshold may

apply to be voluntarily registered. They can register their business on either manual or

online method.

|

What benefits if I register my business under GST?

Our studies have shown that there will be a reduction in the business costs due to:

(i) GST paid on inputs is claimable

(ii) Exports are zero rated

(iii) There is no matching of input tax and output tax

(iv) The existence of special schemes to alleviate cash flow

|

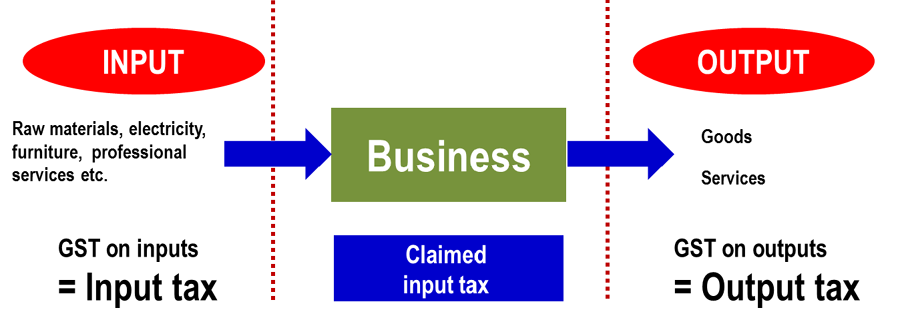

How does GST works?

GST is a tax charged on the supply (including sales) of goods and services made in Malaysia and on

the importation of goods and services into Malaysia. Even though GST is charged on the sales price

of the goods or services, the amount to be remitted to the Government is only on the value added to

the goods or services at each level of the distribution/supply chain. There are three types of

supplies listed under GST which are ‘Standard rated’, ‘Zero rated’, and ‘Exempted’.

|

|

Scenario for how GST works:

Hendry is a computer hardware seller and buy his goods from distributors. He is registered under GST.

I. Standard Rated

Buy a LCD monitor at a price of RM 500.00 and charged 6% GST. The total amount of the invoice is

RM 530.00 inclusive GST. Selling the LCD monitor to his customer at a price of RM 700 and charged

6% GST. The total amount of supply will be RM 742.00.

Output Tax : RM 42.00 (a)

Input Tax : RM 30.00 (b)

--------------------------------

Tax to pay : RM 12.00 (a – b)

His net profit = RM 200 (RM742 – RM530 – RM12)

II. Zero Rated

Buy a LCD monitor at a price of RM 500.00 and charged 6% GST. The total amount of the invoice is

RM 530.00 inclusive GST. Selling the LCD monitor to his customer at a price of RM 700 and charged

0% GST. The total amount of supply will be RM 742.00.

Input Tax : RM 30.00 (b)

Output Tax : RM 0.00 (a)

--------------------------------

Tax claimable : RM 30.00 (b – a)

His net profit = RM 200 (RM700 – RM530 + RM30)

III. Exempted

Buy a LCD monitor at a price of RM 500.00 and charged 6% GST. The total amount of the invoice is

RM 530.00 inclusive GST. Selling the LCD monitor to his customer at a price of RM 700 and charged

0% GST. The total amount of supply will be RM 742.00.

Input Tax : RM 30.00 (b) – not claimable

Output Tax : RM 0.00 (a)

--------------------------------

Tax claimable : RM 0.00

His net profit = RM 170 (RM700 – RM530)

|

|

Please visit the Royal Malaysian Customs Department official website for more information.

|

|